We normally hear some of these common questions:

- How do you invest at all-time high prices in the the stock market?

- Is now a good time to invest?

- Or what should I invest in?

I don’t have a crystal ball so I can’t time the markets (quick tip: no one else does!).

That said, over the long-term investors in stocks have been well rewarded for investing. Whether to invest also depends on your personal situation and when you’ll need the money. Although I don’t have a crystal ball below is our 2020 outlook that discusses what happened in 2019 and thoughts on the future.

2019 Review

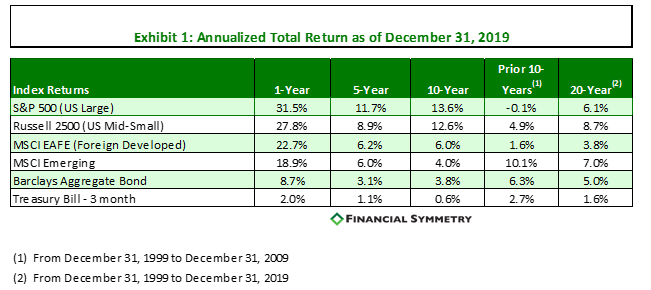

As noted in Exhibit 1, 2019 was an excellent year for stock and bond investors. As a reminder we started 2019 following an ~20% decline in the stock market in the 4th quarter of 2018. There was also significant concern regarding a potential recession, trade war and geopolitical concerns. Very few predicted material gains in the stock and bond markets, but that is the challenge of short-term predictions.

Overall, the last ten years has been an excellent time to invest in large US companies (S&P 500) with an approx. 13.6% return. It may be easy to think all you need to do is invest in the S&P 500, but many forget that during the 2000s the S&P 500 returned -0.1%. We discuss the benefits of global diversification further in our blog post titled, The 2010s: A Decade in Review, but a good chart below (Exhibit 2) showing the differences in returns from the 2000s and 2010s by major equity asset classes.

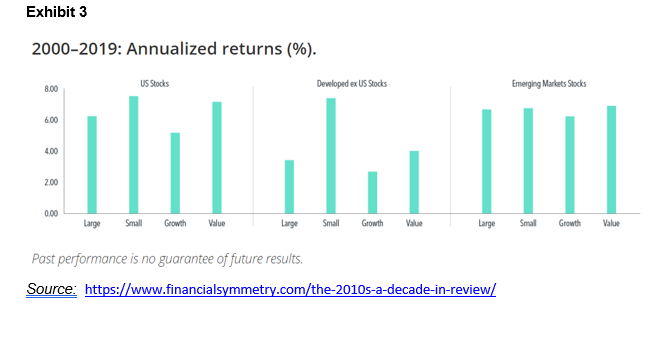

You’ll notice how the winners one decade are typically the losers in the next. In 2010 the common question was why invest in US stocks? Ten years later that question is now why invest in foreign stocks? The answer is over the last twenty years an investor was rewarded for a well-diversified portfolio of US and foreign stocks, rebalanced regularly would have resulted in higher returns than picking one market as noted in Exhibit 3.

Current Situation

At Financial Symmetry, we meet regularly to review different short-term and long-term market indicators to determine the appropriate investment strategy for all our clients.

Below is a brief summary of the current state of a few categories as of the beginning of 2020.

Economy

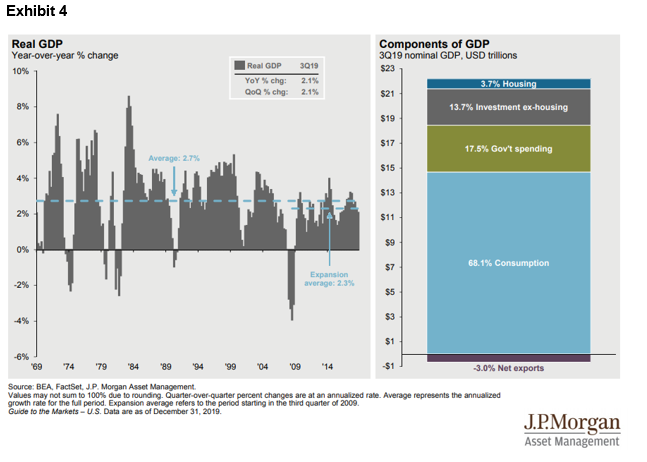

Global economic growth remains below historical levels as concerns remain regarding trade tensions, Brexit, the US presidential election and geopolitical concerns. Although unemployment and inflation remain low in the U.S. overall GDP growth remains below historical levels as noted below with 2.1% growth in the 3rd quarter of 2019. We did see an inverted yield curve in 2019 which has been a consistent indicator of predicting recessions six to eighteen months out, but some would argue current low rates make this time different. Only time will tell. See exhibit 4 below of historical U.S. Real GDP and the key Components of GDP.

Interest Rates

The looser monetary policy by central banks around the world will likely persist in this environment of low growth and low inflation. Market-implied probabilities still slightly favor a U.S. rate cut vs. increase in 2020 but will depend on economic conditions. One benefit of this policy is lower mortgage rates which means it may be a good time to consider refinancing your mortgage if over 4%.

Sentiment

Given the strong recent returns of stocks and low unemployment, consumer confidence remains near the highest levels of the past 20 years. Positive sentiment can drive short-term markets as we saw in the late 90’s but can have a material negative impact when/if it turns. Furthermore, a longer-term measure of sentiment is U.S. households’ exposure to equities. When exposure is high vs. historical standards future 10-year U.S. stock market returns are low and vice versa. Currently, U.S. households have nearly 54% of their assets exposed to stocks, which is in the highest quintile historically – the quintile with the lowest (although still positive) average subsequent 10-year U.S. stock returns. The last times households held this % of stocks were in the late 1990’s and mid 2000’s.

Valuations

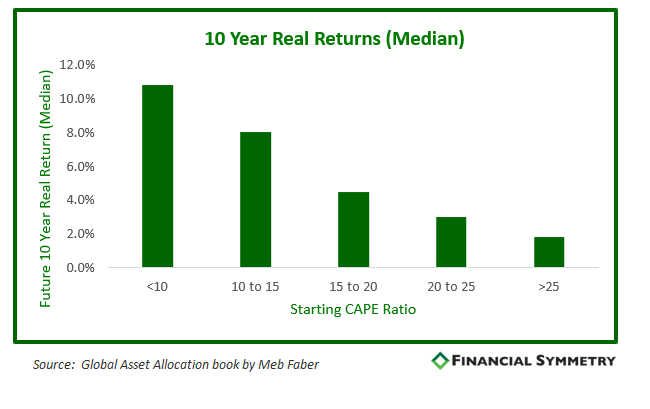

History has found certain periods have resulted in higher/lower returns than others. Part of this can be explained by starting valuation. Valuation is one of the best indicators of long-term returns (i.e. 10 years), but it is a horrible short-term timing strategy. One popular valuation metric we’ve discussed in the past is the cyclically-adjusted price-to-earnings (CAPE) ratio. Instead of dividing price by the past 12 months of earnings, the CAPE ratio divides price by the average inflation-adjusted earnings of the past ten years. The idea is to smooth out the good and bad years created by the business cycle.

In addition, Exhibit 5 below is the average future 10-year real return based on starting U.S. CAPE Ratio. As of December 31, 2019, below are the current CAPE ratios of the major equity markets:

- U.S. Stock Market = 30.8 (96th percentile)

- MSCI EAFE (int’l developed) = 17.3 (36th percentile

- MSCI Emerging = 13.4 (28th percentile)

Source: Research Affiliates

As noted in our blog, Crystal Balls and CAPE, when one market (US or foreign) was trading at a material premium (such as today(U.S.)), the other market stock market outperformed over the subsequent 10-year period.

Exhibit 5

The summary is current stock valuations favor the international markets.

Don’t Forget About Bonds

Regarding bonds our belief is that high quality bonds in your portfolio provide the following benefits:

- Balance – diversification from equities

- Safety – capital preservation

- Income – interest payments

Bond returns are largely driven by the term and credit quality of a bond. Long-term bonds experience bigger price movements for a given change in interest rates. Investor are expected to be compensated for taking that extra risk as a result. The same can be said for lower credit quality bonds such as high yield bonds.

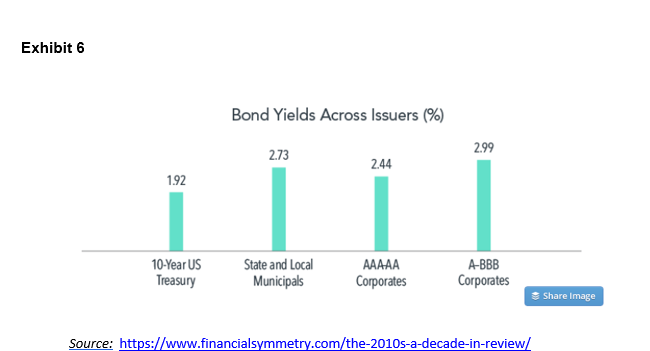

Future returns of bonds are highly correlated to the starting yield. Therefore, as of 12/31/2019 the starting yield on the different areas of the bond market are included in Exhibit 6 below. Overall, yields across all segments of the bond market remain low compared to historical averages so we don’t expect high returns from the bond market over the next ten years. That said, these returns are still expected to exceed cash.

What to Expect

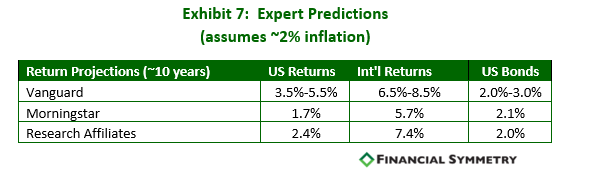

See Exhibit 7 below for projected returns over the ten years from various industry experts for U.S. stocks, international stocks and bonds. Many may ask, “Why bother making predictions since it is so difficult to predict the market’s direction?” Good point over the short-term, but these return expectations are helpful for long-term (~10 years) planning purposes. Note all sources expect higher returns for international stocks than U.S. stocks or bonds. Although we have not listed the specific expectations for Financial Symmetry, our views are similar.

Note: Vanguard and Research Affiliates expect higher U.S. stock returns for value and small company stocks than the U.S. stock returns above. They expect large growth stocks to trail the market over the next 10 year similar to what they did in the 2000’s (see exhibit 2).

Investing at All-Time Highs

To summarize, with lower than average returns expected for U.S. stocks and bonds many investors allocated primarily to U.S. stocks will be disappointed with returns over the next ten years. Although low, these returns are still expected to exceed cash. A globally diversified equity portfolio is recommended, but with potential lower future returns individuals may need to either work longer or spend less than expected to reach their financial goals.

For current savers, a market decline should be viewed positively, as it allows them to buy stocks at cheaper prices. For existing or soon-to-be-retirees, it is important to understand your risk capacity and risk tolerance and adjust your asset allocation accordingly. You’ll need equity for long-term growth, but it is important to have high-quality bonds for short-term spending.

What can you do?

First, focus on what you can control (spending, taxes, estate planning, etc.) and your long-term financial plan. If you don’t have a financial plan in place, it’s the perfect time to contact a fee-only financial planner. Second, implement a long-term, disciplined investment strategy. And no, buying the mutual fund/ETF/stock that has done the best over the last three years is not a strategy. If you don’t have a disciplined strategy or want to learn more about our process, click here.

Outline of This Episode

- [2:27] Short-term market forecasting is impossible to predict

- [5:35] Let’s look at how the markets have performed in the long-term

- [10:52] Take a look at bonds

- [15:10] What has happened with consumer confidence?

- [17:35] Why hold foreign stocks?

- [20:15] What changes should we be making to our portfolios given the current climate?

- [23:54] What do the experts predict to happen over the next 10 years?

Resources & People Mentioned

- Vanguard 2020 Outlook

- Smith Partners Article – Do I Belong Here? All-Time Market Highs and the Good Place

Connect With Chad and Mike

- https://www.financialsymmetry.com/podcast-archive/

- Connect on Twitter @csmithraleigh@TeamFSINC

- Connect on Linkedin: Mike; Chad

- Follow Financial Symmetry on Facebook