It doesn’t seem there should be any difference when calculating investment performance, but there are actually two methods for calculating annualized investment returns. Time Weighted and Dollar Weighted.

When evaluating how a manager has performed, Time Weighted is usually the best approach because a manager often does not have any control over when investors will send them money to invest. Dollar Weighted is usually the best method when an individual investor assesses the performance of their portfolio because they often do have control over when they invest.

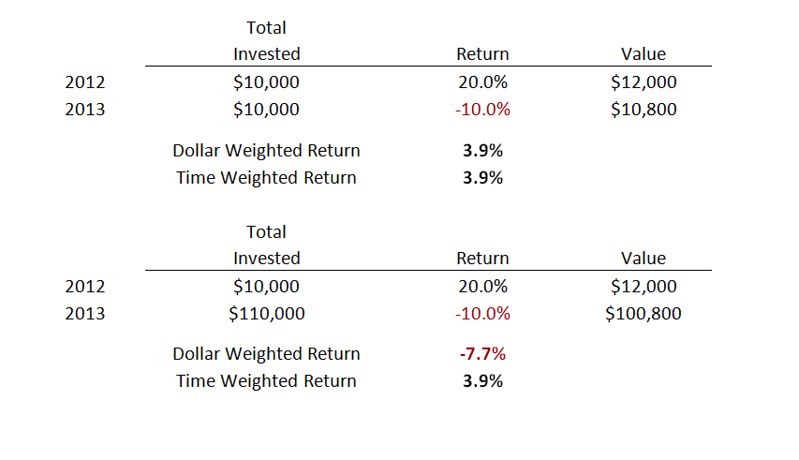

Take for example a hypothetical manager who had returns of plus 20% in 2012 and minus 10% in 2013. If that manager had $1 million in their fund at the beginning of 2012 and no extra money was added, and no money was withdrawn from their fund, then their annualized return for the two years would be 3.9%, and this would be both the Time Weighted and Dollar Weighted return.

Now let’s assume that the manager had $1 million in their fund at the beginning of 2012, but another $10 million was invested at the beginning of 2013. The Time Weighted return for the fund would still be 3.9% for the two years, but the Dollar Weighted return would actually be minus 7.7% because there was much more money in the fund during 2013 when it lost 10%.

Now we can look at the same example, but take it from an individual investor’s perspective. Let’s say that the investor invested $10,000 in the fund at the beginning of 2012 to see how the manager will do, and after earning 20%, they decide to invest another $100,000 in the fund. In this example, the investor was in full control of the timing of their investment and earned plus 20% on $10,000, but then lost 10% the next year after investing an additional $100,000, so they ended up with only $100,800 after investing $110,000 and the Dollar Weighted return of minus 7.7% is a more accurate assessment of the investor’s performance.

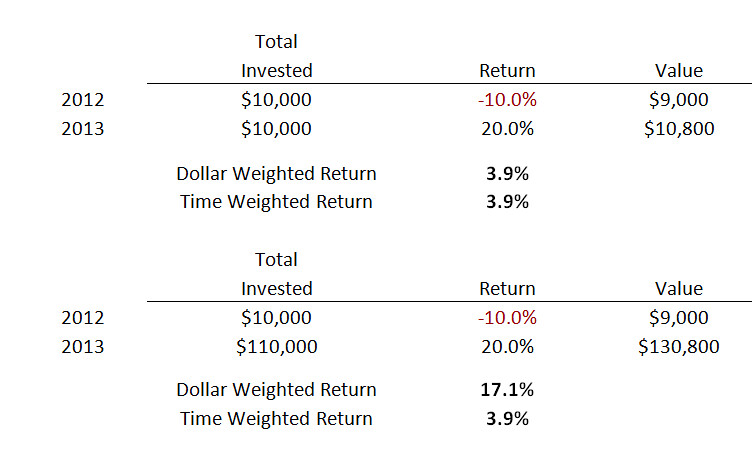

If we take the same example and reverse the sequence of returns so that 2012 was minus 10% and 2013 was plus 20%, then we see that the pattern reverses and the IRR is much higher than the TWR.

If we take the same example and reverse the sequence of returns so that 2012 was minus 10% and 2013 was plus 20%, then we see that the pattern reverses and the IRR is much higher than the TWR.

Morningstar has been tracking Dollar Weighted returns versus Time Weighted returns for all mutual funds, and they have found that over time, investors’ Dollar Weighted returns are significantly lower than funds’ Time Weighted returns which indicates that most investors do a poor job of timing their investments, as they tend to chase returns after they’ve been strong and bail out after losses. For the ten years ending 12/31/2013, the average fund investor’s return (Dollar Weighted) was 2.49% lower than the average fund’s return (Time Weighted).

We have found that a disciplined research and review process is the key to successful investment management. It also seems to be a good idea not to manage your own money which is why all Financial Symmetry advisors have their own Financial Symmetry advisor to review their portfolios.