This is the sixth post in our “What I Wish I Knew About Money as a Teen” series.

Your first paycheck hits, and you’re doing the math, comparing the hours you worked to your salary or hourly rate. You soon notice that your direct deposit is lower than the big number at the top of your pay stub.

Welcome to taxes.

Unless you were lucky enough to take a personal finance course in high school, it’s likely no one explained how taxes affect your life or your paycheck.

Whether you just started your first job or you’ve been filing tax returns for a few years and still feel a little lost, this is the guide we wish someone had handed us earlier.

Why Do We Pay Taxes?

Taxes are mandatory payments to the government. That part probably doesn’t surprise you. But what do they actually pay for?

Roads, schools, hospitals, police and fire departments, Social Security, and Medicare. Basically, taxes help fund the services and programs that keep society running, including some that may support you later in life.

Paying taxes is part of living in a functioning society. In fact, paying more taxes isn’t always a bad thing. It often means you had a good year financially.

The goal isn’t necessarily to pay zero in taxes; it’s to avoid paying more than you legally owe. As your finances become more complex, you’ll also learn that tax planning isn’t just about reducing taxes. It’s about deciding when to pay them. In some years, it may make sense to defer income and delay taxes. In others, it may be beneficial to recognize income and pay taxes now rather than later.

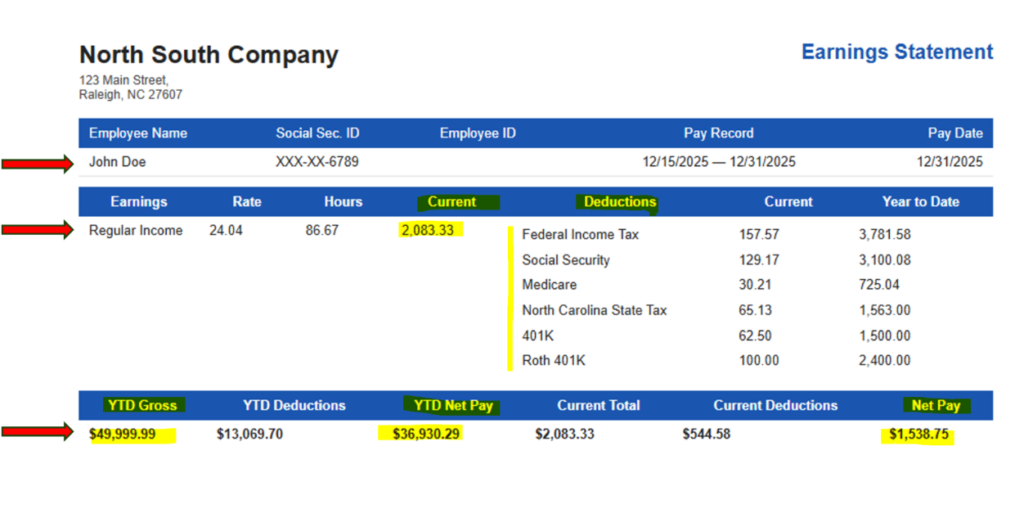

Gross Pay vs. Net Pay

This is one of the first things that trips people up.

Gross pay is the amount you earn before taxes and other deductions are taken out. This could be your annual salary or your hourly wages.

Net pay is what actually lands in your bank account. The difference between the two is taxes and other deductions.

Take a look at your pay stub, and you’ll likely see several items listed:

- Federal income tax: This goes to the U.S. government. The amount withheld depends on factors such as your income, filing status, and the information you provide on your Form W-4.

- State income tax: This depends on where you live and work. Some states have an income tax, while others do not.

- Payroll taxes (FICA): These taxes fund Social Security and Medicare. Most employees pay 6.2% for Social Security and 1.45% for Medicare. Unlike income taxes, these are generally fixed percentages rather than rates that change based on your tax bracket.

Unless you’re self-employed, your employer will generally withhold these taxes from each paycheck and send them to the appropriate government agencies on your behalf.

You may also see deductions that aren’t taxes, such as health insurance premiums, retirement plan contributions, or other employer-sponsored benefits. Some of these deductions can lower your taxable income. For example, traditional 401(k) contributions are often made before income taxes are calculated, which can reduce the amount of income subject to tax while helping you save for retirement.

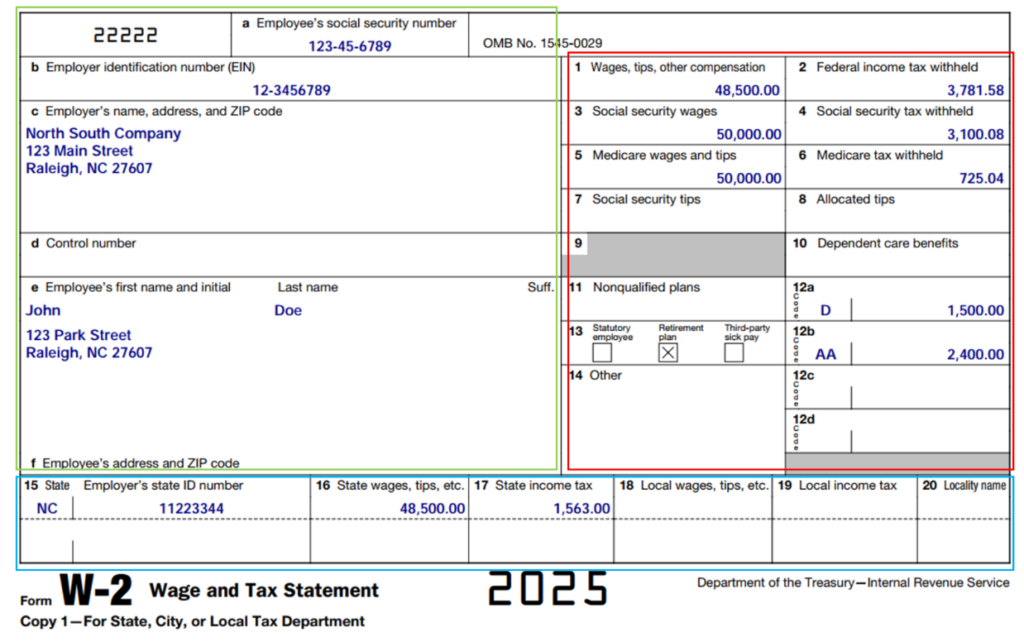

The W-2: Your Year-End Tax Summary

Every January, your employer sends you a Form W-2. Think of it as a report card for your income. It shows how much you earned and how much was withheld from your paychecks during the year.

If you have a traditional job as an employee, you’ll typically receive a W-2. When it’s time to file your tax return, you’ll use the information on that form to report your income and taxes paid.

If you’re also making money on the side through freelancing, babysitting, tutoring, or selling products online, that income may be reported on a different form, such as a Form 1099. Unlike income reported on a W-2, you’re generally responsible for tracking that income yourself and making sure it’s reported on your tax return.

What will your income tax rate be?

Here’s something a lot of people get wrong:

“I don’t want to earn more because it’ll bump me into a higher tax bracket.”

That’s not exactly how it works.

The U.S. tax system is progressive, meaning different portions of your income are taxed at different rates.

Think of it as a series of buckets. The first dollars you earn go into the 10% bucket. Once that bucket is full, the next dollars go into the 12% bucket, then the 22% bucket, and so on.

Only the income that falls into each bucket is taxed at that rate. Moving into a higher tax bracket doesn’t mean all of your income is taxed at the higher rate. It simply means that additional income may be taxed at that higher rate.

Do You Actually Have to File a Tax Return?

Short answer: if you worked, it’s usually a good idea.

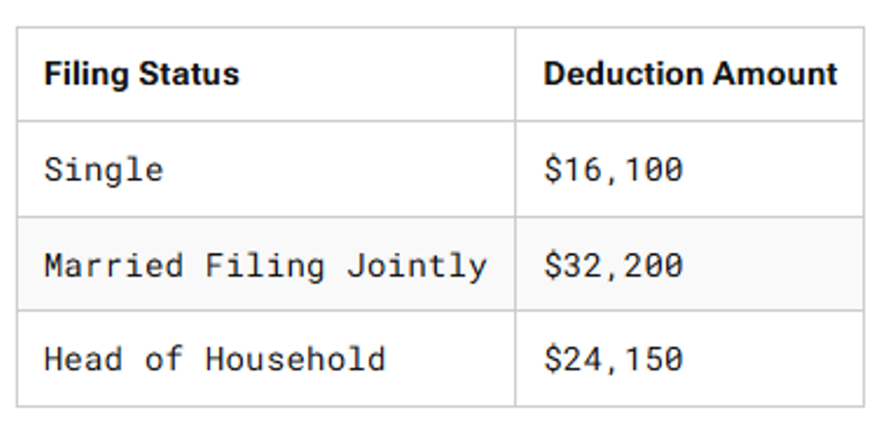

In many cases, you’re required to file a tax return if your income exceeds certain IRS thresholds. One of the most important concepts to understand is the standard deduction, which is a government-set dollar amount that reduces your taxable income.

In simple terms, the standard deduction allows a portion of your income to be excluded from federal income tax. That means some of the money you earn won’t be subject to the tax brackets discussed earlier.

In simple terms, the standard deduction allows a portion of your income to be excluded from federal income tax. That means some of the money you earn won’t be subject to the tax brackets discussed earlier.

Even if you’re not required to file a return, you may still want to. If taxes were withheld from your paychecks during the year, filing a tax return could result in a refund of some or all that money.

If you’re a student or young adult, your parents may still claim you as a dependent on their tax return. That doesn’t mean they report your wages for you. If you earned income, you may still need to file your own tax return.

As for how to file, many people with straightforward situations use tax software such as TurboTax or H&R Block. As your finances become more complex, whether through self-employment income, growing retirement accounts, or starting a family, professional guidance can help you identify planning opportunities and avoid costly mistakes.

The tax filing deadline is typically April 15th of the following year. If that date falls on a weekend or holiday, the deadline moves to the next business day.

What to Take Away From All of This

You don’t need to become a tax expert. You just need to know enough to understand what’s happening with your money and ask the right questions when something doesn’t seem right.

Check your pay stub, file your tax return on time, and take advantage of the benefits available through your employer.

If your tax situation starts to feel complicated or keeps you up at night, don’t hesitate to ask for help. A good financial advisor can help you understand how taxes fit into your overall financial plan and identify opportunities to make your money work more efficiently.

Taxes are a part of life. The better you understand them, the less stressful they become.