Author’s Note: This article was updated on August 4, 2025.

This is a question we usually hear frequently when clients are filling out employment paperwork for a new job or during open enrollment time. Contributions to a 401k have traditionally been pre-tax. In other words, you take a tax deduction on the contribution now, and that money plus earnings is tax-deferred until it is withdrawn in retirement. A recent survey by the Plan Sponsor Council of America showed that 93% of employers now offer a Roth 401k option as well. With the Roth 401k, your contributions go in after tax, so you don’t get the tax deduction now, but you will be able to make tax-free withdrawals from that money, plus earnings, in retirement. Any employer contributions, however, will still be considered pre-tax contributions and subject to ordinary income tax upon withdrawal.

While we almost always recommend contributing enough to your 401k to receive the full employer match, the percentage to contribute and whether to do traditional or Roth contributions are highly situation-specific. Before deciding whether you should put those hard-earned dollars to work in a traditional or Roth 401k, you should ask these 5 crucial questions:

What Is My Current Tax Bracket?

If you are in the 0, 10, or 12% tax bracket, then it is likely you will benefit from contributing to your company’s Roth 401k. At these income levels, assuming your income will grow over time, it is likely you will be in a higher tax bracket at some point in the future. There is also the potential that these very low tax rates will increase in the future, so taking advantage of paying taxes on these funds now at a very low rate, allowing the funds to grow tax-free, and making tax-free withdrawals in retirement is likely a good bet.

If you are in the 22% tax bracket or higher, then the answer is not quite so clear-cut. At these tax rates, you want to do a closer analysis of what other tax benefits you might be missing out on by pulling that money into taxation now. For example, the capital gains tax rate for taxpayers in the 0, 10, and 12% brackets is 0%. Therefore, pre-tax contributions that reduce your taxable income to these levels could allow for additional savings. You will also want to consider your eligibility for Education, Child Tax Credits, and other deductions that are based on your Adjusted Gross Income. In many cases, higher-income earners get more bang for their buck with traditional pre-tax 401k contributions.

What Do I Expect My Tax Bracket to Be in Retirement?

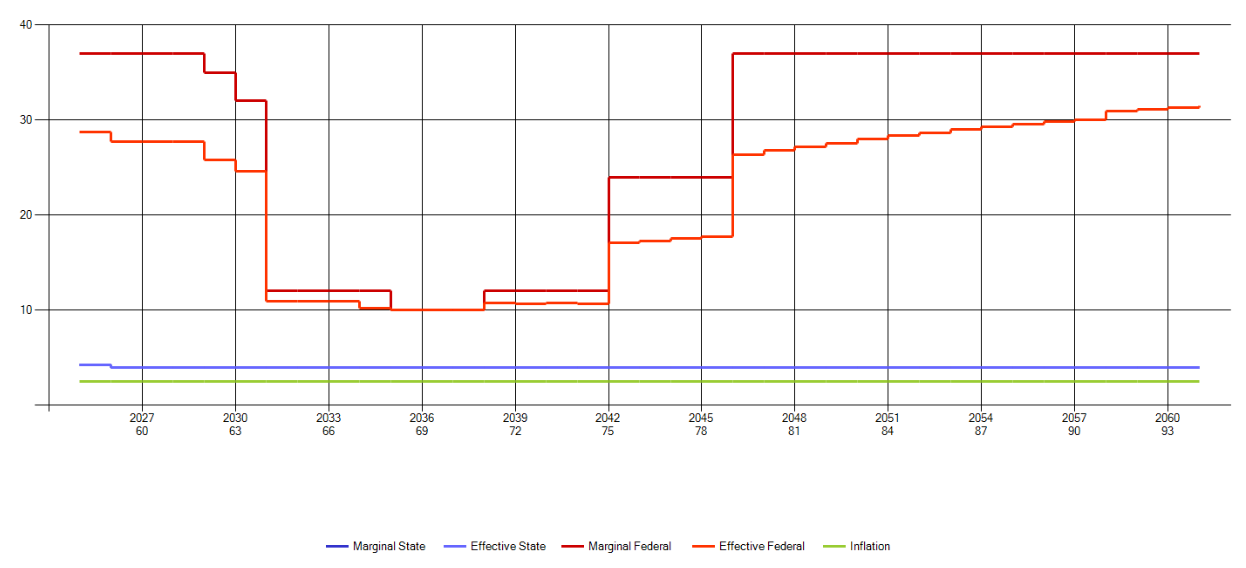

This is a tricky one, as you don’t have a crystal ball. However, looking at a financial projection can be helpful. In many cases, we find that clients who retire early, prior to drawing Social Security, will see a significant drop in their tax rate. This can be quite dramatic and beneficial from a tax planning perspective. For example, if you are earning $250k/year now (Married Filing Joint), but plan to retire at age 60, your tax bracket may drop from 24% to 12% or even lower in the years between retirement and the date you begin Social Security. For example, in early retirement, it’s not uncommon for your tax bracket to follow a pattern like this:

These years pose the potential for huge tax savings as capital gains can be realized at the 0% rate or traditional 401k, or IRA money can be converted to Roth. The Roth conversion can now grow completely tax-free, which offers numerous benefits like:

- Withdrawals will be tax-free later in retirement when your tax bracket likely rises again with the addition of Social Security Income and Required Minimum Distributions.

- Your RMDs will be smaller since conversions will reduce your base account value, and Roth IRAs are not subject to RMDs.

Once you start drawing Social Security, the Social Security Tax Bubble needs to be taken into account, limiting the potential benefit of a low tax bracket, so it is critical to be proactive about planning ahead for this retirement tax window.

What Is My Future Income Potential?

If you are just getting started in your career and expect your income to grow, this is likely the time to take advantage of the Roth 401k option. The earlier you can start making contributions, the longer those funds grow tax-free. When your income rises, you can split your contributions between traditional and Roth, adjusting more to traditional for the tax benefit as your income grows. This is also something to reevaluate as life changes occur, for example, if one spouse leaves the workforce to care for young children or aging parents.

Can I Contribute to a Roth IRA?

The Roth IRA is the gold standard of retirement savings accounts. Contributions go in after-tax, earnings grow tax free, and withdrawals are completely tax free in retirement. And did we mention that you can always withdraw your contributions tax and penalty-free? These provisions allow for ultimate flexibility in your savings and investment strategy. The catch is you can only make full contributions if your Adjusted Gross Income is below the phase-out ranges ($236-246k MFJ; $150-165k Single). If your income is on the border of these ranges, contributing more to your traditional 401k may bring you into Roth eligibility. This would allow you to save taxes now by making pre-tax contributions to your 401k and contribute to Roth IRAs, saving you tax dollars later. We call this tax diversification. It gives you options and flexibility, which puts you in a strong position to take advantage of changes that come your way. If your income is above the phase-out ranges, there still may be an option for you to get into a Roth IRA.

What Are My Other Savings Strategies?

Retirement is not the only goal you are saving for. Saving in your 401k is great, and we encourage our clients to max out their contributions to the best of their ability. However, our lives are filled with competing goals like:

- Meeting day-to-day cash flow needs like mortgage and daycare payments

- Vacations

- College tuition

- Weddings

- Home improvements

Most of these items cannot be paid for with money inside your 401k plan, at least not easily while you are working and prior to age 59 ½. That’s why it’s difficult to answer the question of Roth or traditional 401k in a vacuum.

Building an appropriate emergency fund and taxable savings is also important. After all, that is what helps us cover those unexpected expenses as well as save for the more tangible short and intermediate-term goals. Building these funds also allows you to take advantage of the additional tax savings opportunities as mentioned above. Therefore, it’s important to make the Roth/traditional 401k decision in the context of your overall financial plan.

If you have questions specific to your situation, please set up a time to talk with one of our advisors.

Copyright: designer491 / 123RF Stock Photo