This is the fourth post in our “What I Wish I Knew About Money as a Teen” series.

In previous posts in this series, we’ve introduced several foundational concepts for improving financial literacy—creating an emergency fund, budgeting and saving, building credit, and managing debt. If you have been following along, ideally, your emergency savings account balance is sufficient, you have consistently managed to stick to a proper budget, and you know what it means to avoid bad debt. Naturally, you may be wondering: What’s next? Should you simply continue to stash money in your savings account?

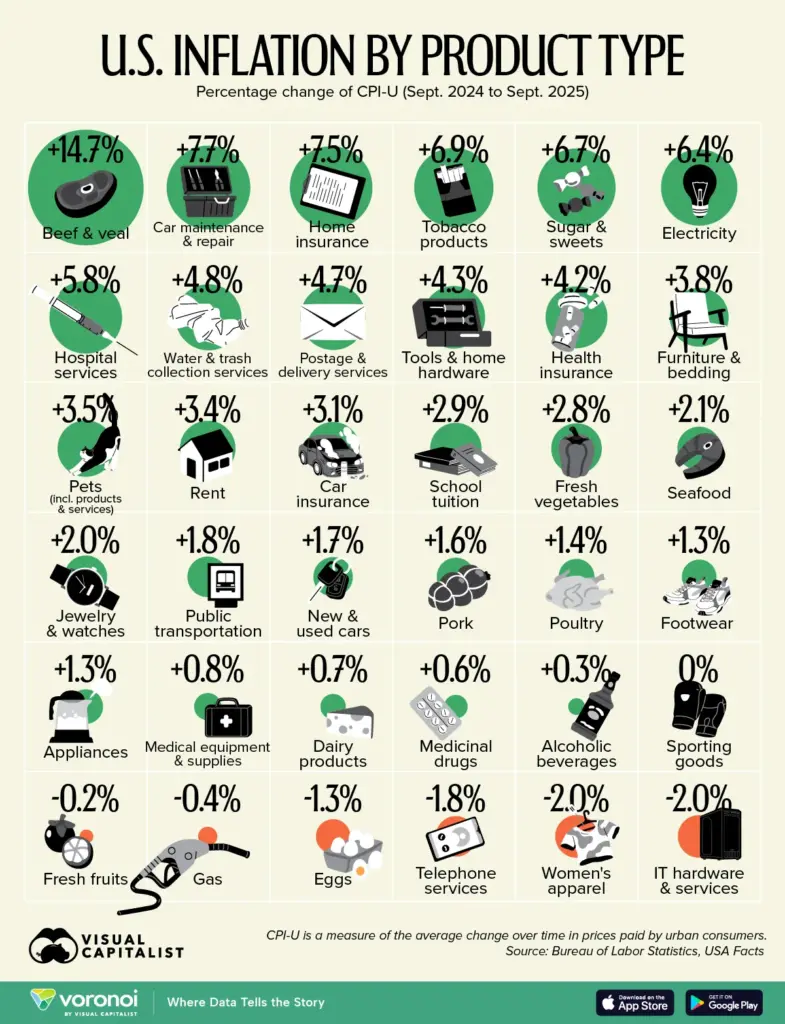

It is common, human nature even, to perpetually stockpile cash for a rainy day. We crave stability and despise uncertainty. But eventually, cash stops being “king.” Savings are crucial for short-term anticipated expenses and unexpected setbacks. Beyond this, however, purchasing power is eroded by inflation, and even the highest-yielding savings accounts struggle to keep up. Consider, for example, the U.S. inflation by product over the course of September 2024 to September 2025:

Source – https://www.visualcapitalist.com/visualized-u-s-inflation-by-category-in-2025/

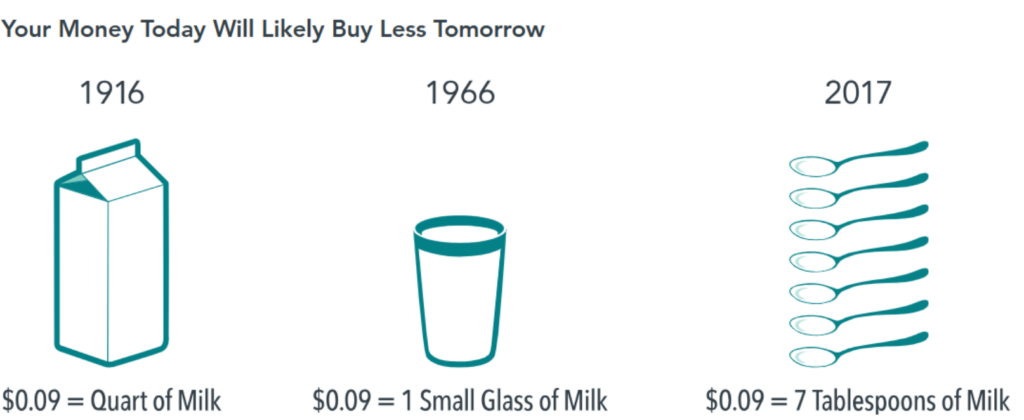

Or to see inflation’s impact at scale, review comparative pricing for milk, from 1916 to 2017:

Source: https://my.dimensional.com/impact-of-inflation

Continuing with our series, I wish I knew many things about money as a teen, such as the existence of inflation and its ravaging effect on your hard-earned funds. Before beginning to invest, it’s helpful to first understand the force it’s designed to counteract. Inflation varies from year to year, but in America it has lingered around 2% annually. This means that a basket of goods costing $100 today will, on average, cost you $102 the following year. Over small time periods, this increase seems trivial, but compounding can work against you just as much as it works for you.

Excessive cash as a percentage of one’s assets can wreak havoc on long-term goals and overall retirement planning. Cash left idle in a savings account for decades, rather than invested, ultimately loses value. What costs $100 in year one (today) will cost approximately $145.68 in year 20 – a 45.68% price increase! At scale, this concept is truly astounding.

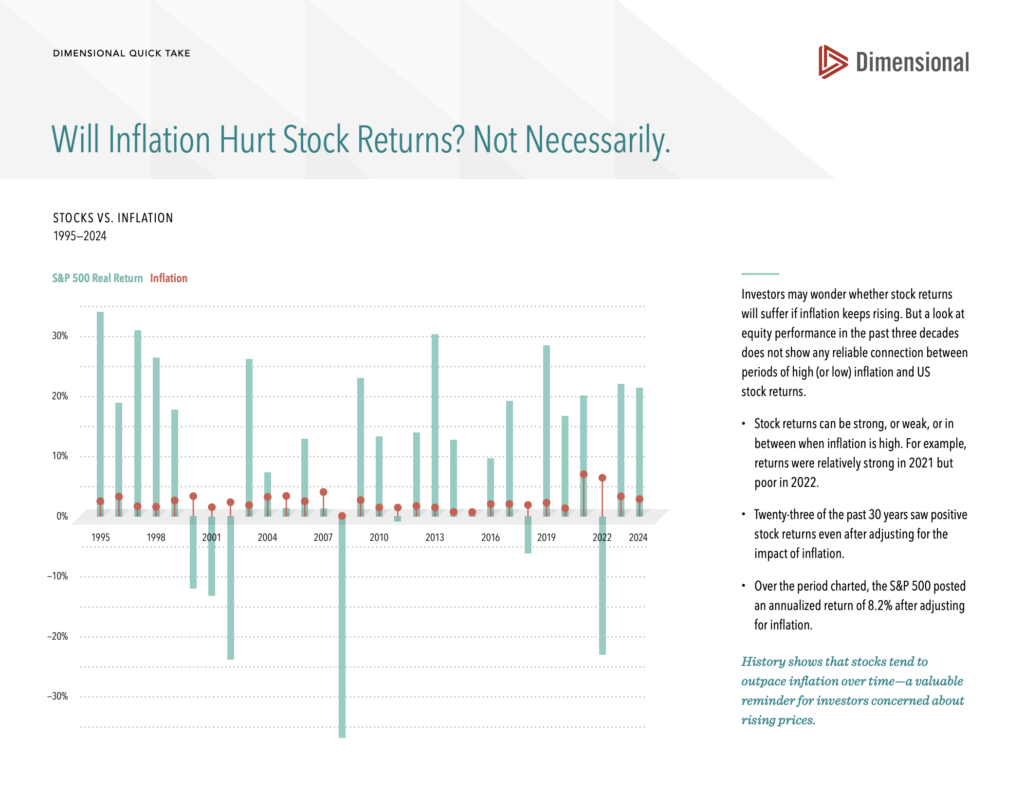

By contrast, from 1995 – 2024 the U.S. stock market generated a return of 8.2% per year (post-inflation).

Though not guaranteed in the future, money invested in companies has tended to outpace surging prices. But being an investor means accepting a trade-off: increased day-to-day fluctuations in your account values (both up and down) in exchange for higher expected returns. The alternative seems more comfortable — keep assets in cash, with the assurance that the amount in your account will remain the same (aside from interest earned, of course). However, this is arguably the riskier route, knowing that the real value of that cash will decline over time.

Coming Next in the Series

When I was younger, if I had known that leaving my funds in cash would come at an invisible cost, I would have been far more motivated to invest sooner. And this leads to my next wish: having an earlier introduction to the concept of diversified investing. Knowing that you should invest is one thing, but it is another entirely to understand how to start.

Investing doesn’t have to feel terrifying or overwhelming.

In our next post, we will cover the basics of investing and what it means to build a diversified portfolio. Until then, feel free to share this article with others if you have found it helpful!