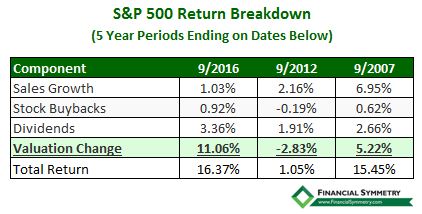

During 2011, in the midst of the federal debt showdown, there would have been very few investors who believed the S&P 500 would return 16% per year over the next five years, especially if they knew that company economic performance would only increase by 5%. Why did the stock market do so much better over the last 5 years (period ending Sep 2016) than the actual economic performance of the companies that make up the index?

The answer is expanding stock market valuations. In other words, stock prices have risen; and by more than what would be justified by earnings and sales growth.

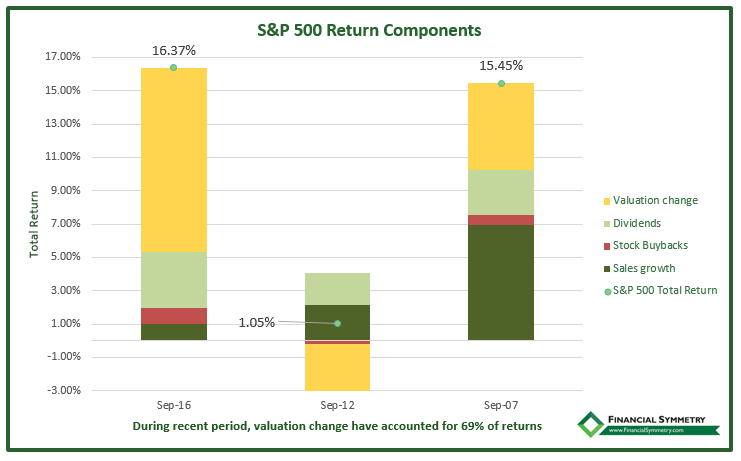

The expansion of valuations made up 69% of the returns!

Valuation Expansion vs. Other Growth

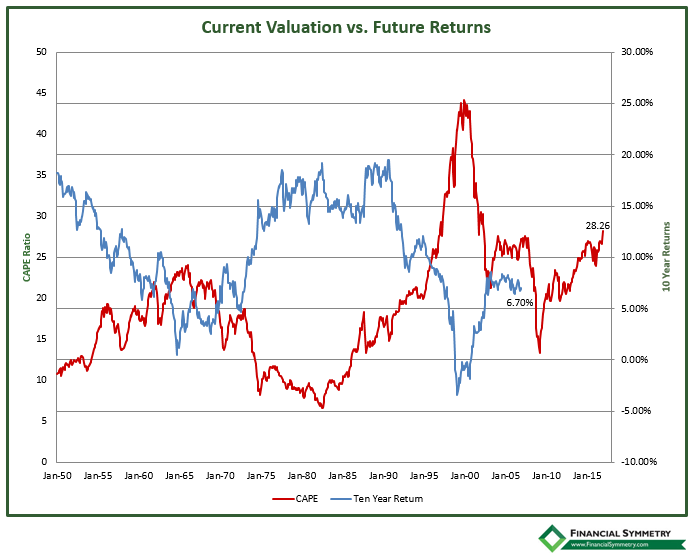

For a recent comparison we can look at the period that preceded the last time valuations were at the levels we are seeing now. This was September 2002, when the valuation measurement tool known as the CAPE ratio was at 22 for the S&P 500, which is not cheap by historical standards but still well below the 28+ that we are seeing in the most recent calculation.

For the next five years, total returns on the S&P 500 averaged 15.45% and at the end of September 2007 the CAPE ratio ended at a robust 27. However, the components of S&P 500 economic performance during that period were quite a bit different than what we’d seen over the recent five years. Sales growth was a healthy 7% compared to the 1% we have seen in this slow growth environment.

As a contrast, the next five years ending September 2012 saw the CAPE fall back to basically the same level it was 10 years earlier in September 2002. Total returns were only 1.05% on the S&P 500 while sales growth fell to a much lower rate of 2%. Of course during this period there was a generational bear market (aka The Great Recession) that took over 50% off of the S&P 500 Index price from top to bottom. For the full decade, total returns on the S&P 500 were 8%, but it was feast and then famine to get there.

Knowing that we are at valuation levels that are now greater than levels that immediately preceded such a tremendous loss in stock market value is why we have been reducing US stocks during this later phase of a very extended bull market.

Influence of Cycles on Valuations

Valuations go through cycles, they expand for a period of time and then contract for period of time as you can see from the change in the CAPE Ratio (red line) in the chart below. The CAPE is a valuable tool for predicting long term stock returns. The chart compares how the performance of the S&P 500 (blue line) has fared over the following 10 years from starting CAPE levels. This is particularly evident when the CAPE has gone to extreme levels as was the case in the early 80’s (hyper-inflation from 1970s) and tech bubble of the late 1990s/early 2000s. The last time that valuations were as high as they are now in the US market was in 2007 just prior to the housing/credit bubble collapse.

Discipline Remains Paramount

The lesson – it’s important to understand the how of market results especially when times have been good. Looking at past results will have powerful influences on our thought process without discipline. Recency bias and the fear of missing out after supersized returns can drive us to harmful emotional decision making. This is when disciplined investing becomes even more important. Because as often is the case in investing, you don’t realize you’re making mistakes until after the fact.